.png)

E-bike retailers operate in a space where technology, physical products, and customer experience all intersect. Sales often happen online, through websites or mobile platforms. These systems handle personal information, payment details, and order histories.

As with many modern retail businesses, the use of digital tools increases exposure to cyber threats. Cybercriminals target businesses that store customer data, accept online payments, or operate cloud-based systems. E-bike businesses are no exception.

Cyber insurance helps manage the risks that come with operating digitally. This guide outlines how cyber insurance works, what it covers, and how it connects to the unique needs of e-bike retailers.

Why Cyber Insurance Matters for E-Bike Retailers

Cyber insurance is a type of commercial insurance that helps cover financial losses related to cyber incidents. These incidents include data breaches, ransomware attacks, phishing scams, and system outages. Cyber insurance may also cover costs tied to legal claims, customer notifications, and restoring compromised systems.

E-bike retailers collect and store customer names, emails, phone numbers, addresses, and card payment information. These details are sensitive and can be targeted by attackers. Many e-bike businesses also use inventory and point-of-sale systems that are connected to the internet, which increases the risk of unauthorized access.

Small and mid-sized retailers are frequent targets of cyber attacks. Without cyber insurance, costs from these incidents are typically paid out of pocket.

Key points:

- Digital Vulnerability: E-bike retailers store customer personal and payment data through online platforms and digital sales systems

- Financial Protection: Cyber insurance helps pay for expenses linked to cyber incidents, including system recovery and legal support

- Regulatory Compliance: Businesses that collect personal data may need to follow privacy regulations

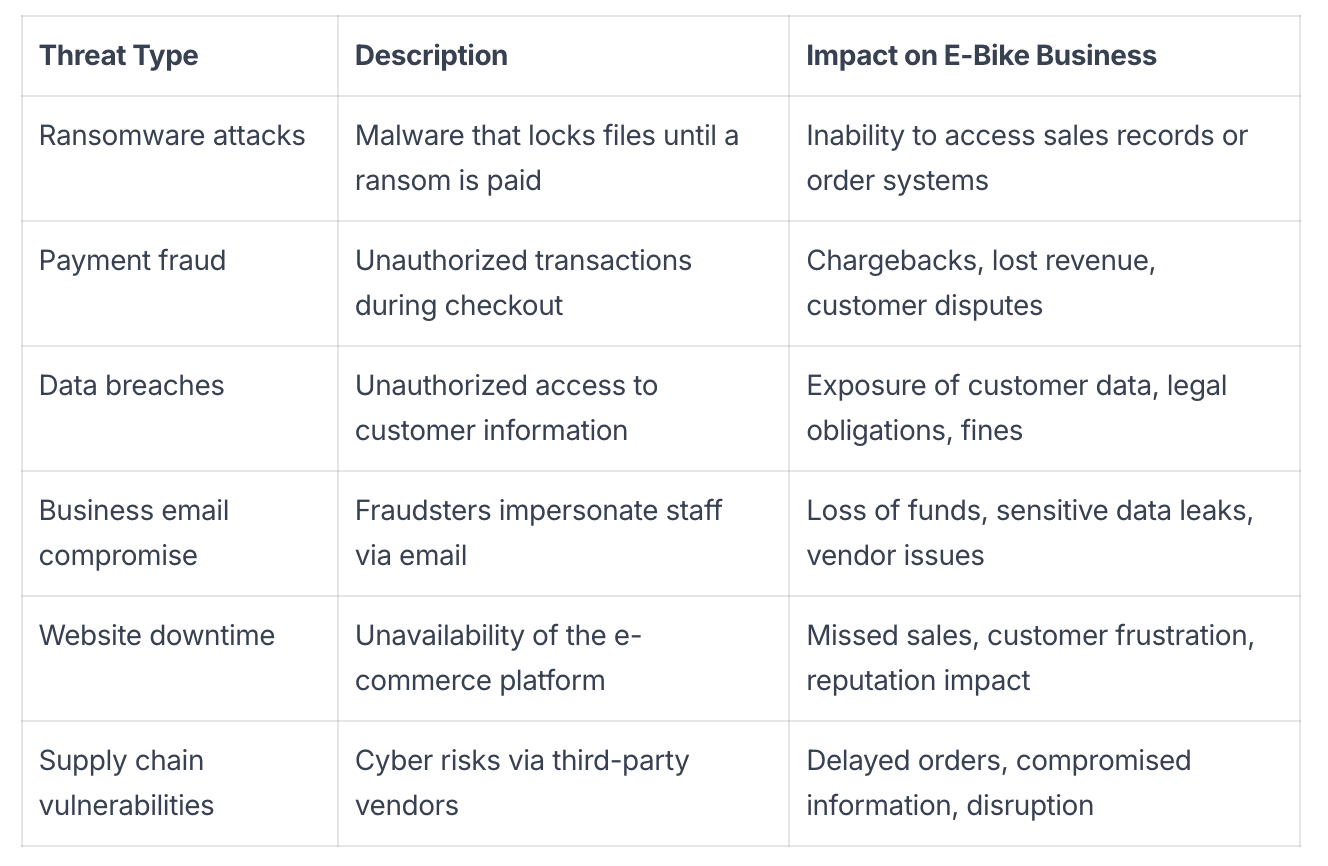

Key Cyber Threats Faced by E-Bike Retailers

E-bike retailers rely on digital tools to sell products, manage inventory, and communicate with customers. These activities create opportunities for cyber threats. Cyber incidents can interrupt business operations, expose sensitive information, or lead to financial loss.

Common threats to e-bike retailers include unauthorized access to systems, fraudulent transactions, and disruptions to online platforms. Each threat type has specific consequences and may be addressed using technical controls, staff training, or vendor management.

The following table outlines key cyber threats relevant to e-bike businesses:

Cyber threats evolve over time. Regular assessments help identify areas of improvement for e-bike retail cyber security.

Core Coverage Areas of a Cyber Insurance Policy

Cyber insurance policies for e-bike retailers protect against losses caused by digital incidents. These policies vary, but there are four common components typically found in comprehensive coverage.

First-Party Liability

First-party liability refers to costs the e-bike business faces directly when a cyber incident occurs. It typically covers expenses such as data restoration, lost income due to systems being down, and hiring IT specialists to fix affected systems.

For example, if an e-bike store's website is attacked and customer data is lost, the business may need to recover its database and pause online sales. First-party coverage can help pay for the recovery process and cover lost income while the website is offline.

Third-Party Liability

Third-party liability applies when another person or business claims harm because of a cyber incident involving the e-bike retailer. This coverage often includes legal defense costs, court fees, and settlements if the business is found responsible.

If customer data is exposed in a breach and a customer files a lawsuit, third-party liability can help cover legal expenses and any required payouts from the case.

Data Breach Response

Data breach response coverage includes services and costs needed to respond after customer information has been compromised. Common areas covered include:

- Forensic investigation to find out how the breach happened

- Notification services to alert affected customers

- Credit monitoring for affected individuals

- Public relations efforts to manage the situation

These elements help the business act quickly and comply with legal obligations while also maintaining trust with customers.

Regulatory and Legal Protection

This coverage supports e-bike retailers when they face investigations or penalties from government authorities. Many privacy and data protection laws require businesses to meet specific standards when storing or handling personal data.

Cyber insurance may cover legal representation during investigations, as well as fines or penalties when allowed by law. This helps businesses meet compliance requirements and manage legal costs after a breach.

How Cyber Coverage Integrates With Other Insurance

Cyber insurance addresses risks related to data breaches, cyber attacks, and digital operations. It works alongside other business insurance policies that e-bike retailers often carry.

General liability insurance: This policy covers bodily injury and property damage that happens to third parties, such as a customer slipping in the store. It does not cover digital incidents like hacking or stolen customer data.

Property insurance: Property insurance protects physical assets, such as e-bikes, inventory, and store fixtures, from risks like fire or theft. It does not cover electronic data, software, or losses caused by cyber attacks.

Professional liability insurance: This policy covers claims related to professional errors or omissions, such as giving incorrect advice. It does not include losses from a cyber breach unless the breach results from a professional error.

Business interruption insurance: Business interruption coverage pays for lost income when business operations stop due to events like fire or flood. It usually excludes interruptions caused by cyber events unless specifically endorsed.

Practical Steps to Reduce Cyber Risks

Cyber insurance helps cover costs after a cyber incident, but it works best when paired with steps that lower the chance of a breach. Some insurance providers also offer lower premiums to businesses that follow cybersecurity best practices.

1. Perform Regular Security Audits

A security audit is a review of a business's digital systems to find weaknesses that attackers could use. For an e-bike retailer, this includes checking the security of point-of-sale systems, website platforms, customer databases, and employee devices.

Quarterly audits are a common standard, but smaller businesses may conduct them twice a year. Affordable audit tools include cloud-based scanning software or third-party services that specialize in small business cybersecurity.

2. Train Employees on Cybersecurity

Cybersecurity training helps employees recognize and avoid common threats, such as phishing emails, weak passwords, and unsafe websites. E-bike retail staff who handle customer data or payment information can learn about secure checkout procedures, laptop security, and how to report suspicious emails.

Training sessions can occur every six months and be updated when new threats emerge. Online courses from non-profit organizations or government portals are helpful resources.

3. Use Strong Data Protection Methods

Protecting customer data is essential for e-bike retailers. Two important methods include:

Multi-factor authentication (MFA) requires users to provide two or more pieces of information before accessing an account. This often includes something they know (a password) and something they have (a code sent to their phone).

Encryption turns payment data into unreadable code when it is stored or transmitted. This means if the data is stolen, it cannot be used without the decryption key.

E-bike retailers that accept credit card payments are required to meet Payment Card Industry Data Security Standard (PCI DSS) compliance. This includes using encryption on all cardholder data.

4. Create a Response Plan

A response plan outlines how a business will identify, respond to, and recover from a cyber incident. For e-bike retailers, this includes steps for detecting a breach, containing the issue, notifying affected parties, and restoring systems.

Key components include a contact list of decision-makers, roles and responsibilities, backup procedures, and guidelines for communicating with customers. Having a documented plan may also be a requirement for some cyber insurance policies.

Frequently Overlooked Costs of a Data Breach

When e-bike retailers experience a cyber breach, several indirect or hidden costs can follow. These costs are not always obvious at the outset but can significantly affect the business:

- Customer notification expenses: Laws require businesses to notify individuals if their personal data has been compromised

- Forensic investigation costs: Specialists may be needed to determine how the attack occurred and what data was accessed

- Legal consultation fees: Legal counsel is often required to assess liability and respond to regulatory investigations

- Public relations management: Managing reputation following a data incident includes public statements and media inquiries

- Business downtime losses: Revenue may be lost if the website or point-of-sale system is offline due to a breach

- Customer compensation: Some businesses offer affected customers refunds, discounts, or free credit monitoring services

- Reputation damage: Trust may be reduced if customers believe their personal information is not secure

Empowering E-Bike Businesses With Comprehensive Protection

Cyber insurance is one part of a broader risk management plan for e-bike retailers. It offers financial coverage for cyber-related losses and works alongside other types of insurance to protect the full scope of business operations.

Business continuity depends on quickly managing incidents that disrupt digital systems. Cyber insurance helps cover recovery costs so that operations can resume with fewer delays. It also supports legal compliance and public response, which are necessary steps after a data breach or cyberattack.

Retail-specific insurance providers understand the unique risks of selling e-bikes online and in-store. These providers can help identify gaps in coverage and suggest policies that match business processes.

At Summit, we understand the cyber risks faced by e-bike retailers across Canada. Get a personalized insurance quote tailored to your specific business needs here.

FAQs About Cyber Insurance for E-Bike Retailers

What does cyber insurance typically cost for a small e-bike retailer?

Cyber insurance for a small e-bike retailer in Canada typically ranges from $500 to $2,500 annually. Pricing depends on factors like revenue, data storage practices, number of employees, and online sales volume.

How does cyber insurance protect against payment processing breaches?

Cyber insurance can cover the costs of investigating payment system breaches, notifying affected customers, and restoring compromised systems. It may also include coverage for legal expenses related to exposed financial data.

Do e-bike retailers need cyber insurance if they use a third-party payment processor?

E-bike retailers can still be held responsible for customer data breaches, even when using third-party processors. Cyber insurance can help address liability gaps not covered by the third party's policies.

How quickly can cyber insurance coverage be activated after a data breach?

Coverage activation depends on the insurer and the policy terms, but claims support often begins within 24 to 72 hours after an incident is reported. Some insurers offer immediate response teams for urgent breaches.

What information do e-bike retailers need to provide when applying for cyber insurance?

Retailers are typically asked to provide details about their annual revenue, number of customer records stored, website operations, current cybersecurity measures, and past incident history.

.png)